The Federal Accounting and Standards Board (FASB) created the new lease accounting standard (ASC 842), which has raised questions about how balance sheets are affected. We’ve answered your top 10 questions about how ASC 842 will impact your balance sheet. Below, we break down the top questions about ASC 842 and what they mean for your financial reporting.

As you navigate these requirements, the right system can make compliance far easier. Visual Lease helps organizations manage lease data, streamline reporting and maintain audit-ready ASC 842 compliance.

What is the purpose of the FASB lease accounting changes?

FASB ASC 842 increases disclosure and visibility into the leasing obligations of both public and private organizations.

Prior to ASC 842, most leases were not included on the balance sheet. The new standard requires companies to report right-of-use (ROU) assets and liabilities for almost all leases. The changes make it easier for users of financial statements to see a company’s exposure to risk and the true financial position of the organization, and to make comparisons between organizations.

Another important purpose of ASC 842 is to more closely align with the new international lease accounting standard (IFRS 16), especially around the definition of a lease.

Public sector organizations often manage diverse lease portfolios and face added scrutiny around transparency and reporting. Learn how Visual Lease supports local governments and public universities with the tools to maintain accurate records and stay compliant with ASC 842.

1. Are operating leases and leased assets on the balance sheet?

Under the ASC 840 standard, only accounting for capital leases were recorded on the balance sheet. Operating leases were off the balance sheet, and the impact was generally limited to deferred rent or prepaid rent. The only insight you had for future obligations was limited to the maturity analysis in the disclosure report. Leased assets under operating leases were not represented on the balance sheet, which often led to an incomplete picture of a company’s financial position.

Under ASC 842, every lease (with the exception of short-term leases) must be represented on the balance with a liability and a ROU asset. This means that leased assets are now recorded as ROU assets, reflecting a company’s control over the leased property for the lease term. The ROU asset is initially measured based on the lease liability, adjusted for any lease incentives, initial direct costs, and prepayments. This change provides a more transparent and comprehensive view of a company’s financial position.

Additionally, disclosure reports must include more qualitative and quantitative disclosures under 842, such as weighted average discount rate, weighted average remaining lease term, cash paid for amounts included in lease liabilities, and a more descriptive maturity analysis (which must be tied back to the balance sheet).

Operating leases vs finance leases under ASC 842

Under ASC 842, leases are classified as either operating or finance leases, each with distinct accounting treatments. While both types require recognition of a right-of-use (ROU) asset and a lease liability on the balance sheet, their expense recognition differs. Finance leases result in front-loaded expenses due to separate interest and amortization costs, while operating leases maintain a straight-line expense profile over the lease term. Proper classification heavily impacts financial metrics, making it essential for companies to carefully assess lease terms and conditions.

2. How are ASC 842 short term leases and low value leases defined?

Under ASC 842, a short-term lease is defined as a lease that has a term of 12 months or less at commencement, and the lease does not have a renewal option that the lessee is reasonably certain to exercise.

Short-term leases do not need to be included on your balance sheet under ASC 842. However, you may recognize short-term lease payments on a straight-line basis over the lease term (similar to the way operating leases are recognized under ASC 840).

This practical expedient for short-term leases must be elected at the asset class level. That means you can’t pick and choose leases to define as short term; you’ll need to define the entire asset class as part of your practical expedient.

It’s also important to note that FASB has not defined a materiality threshold (where low value leases under a certain threshold may be excluded). IFRS (the international standard) has defined a low value lease threshold under which leases don’t have to be capitalized on the balance sheet, but FASB has not included this practical expedient to date. We recommend discussing the issue with your auditors to determine if they will allow you to use a materiality threshold.

3. How are capital leases reported on the balance sheet under ASC 842?

A finance lease (previously called a capital lease in ASC 840) is a lease that’s effectively a purchase arrangement.

ASC 840 capital leases and ASC 842 finance leases are substantially the same. Both are capitalized on the balance sheet, and the method for doing so is similar under both standards.

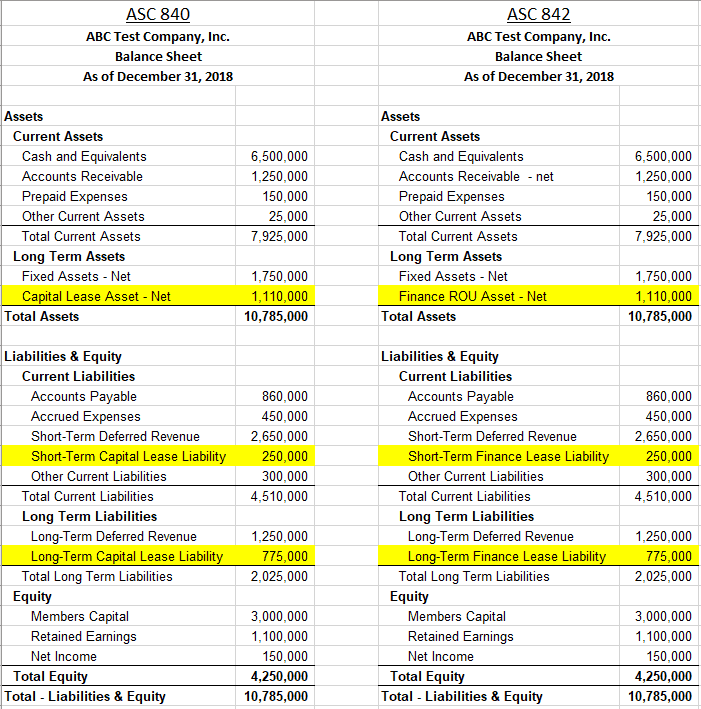

ASC 842 Lease Accounting Example

Here’s an example of a balance sheet for 840 and a balance sheet for 842. Both represent the same capital/finance lease data.

As you can see, only the terminology has changed. Total assets and liabilities remained the same for the reporting period. If we were to look at the income statement, the amortization and interest expense are calculated the same way in ASC 842 as they were in ASC 840. So there would be no impact to the P&L in this example.

When transitioning your existing leases to the new standard, you will need to reclassify Capital Lease Asset and Capital Lease Liability (840) to ROU Asset and Lease Liability (842). Any prepaid rents, lease incentives, and initial direct costs are rolled up into the ROU asset. (Refer to question 8 for more details about calculating the ROU asset).

Need help keeping every detail accurate across your lease portfolio? Explore how Visual Lease’s lease accounting platform centralizes lease data and ensures every asset and liability is accounted for correctly.

4. How are operating leases reported on the balance sheet under ASC 842?

In an operating lease, the lessee obtains control over the use of the underlying asset without ownership. (Refer to question 9 for information about how to classify a lease as either an operating lease or a finance lease for ASC 842 reporting.)

Under ASC 840, operating leases were unrecorded liabilities. Balance sheet impact for operating leases was limited to prepaid or deferred rent.

Accounting for operating leases represents the biggest change in ASC 842, and it will materially impact your balance sheet going forward.

All operating leases (except for short-term leases) are now capitalized on the balance sheet for FASB 842 the same way we previously would record capital leases under ASC 840, and now finance leases under ASC 842. They are recorded on the balance sheet as a ROU asset and lease liability.

Operating lease expense is still straight-lined over the lease term:

- Operating lease liability is accounted for the same way as a finance lease, using an amortized cost basis.

- Amortization of the ROU asset is calculated as the difference between straight line rent and interest expense for the period.

These two expenses added together give you the total lease expense to book on your P&L.

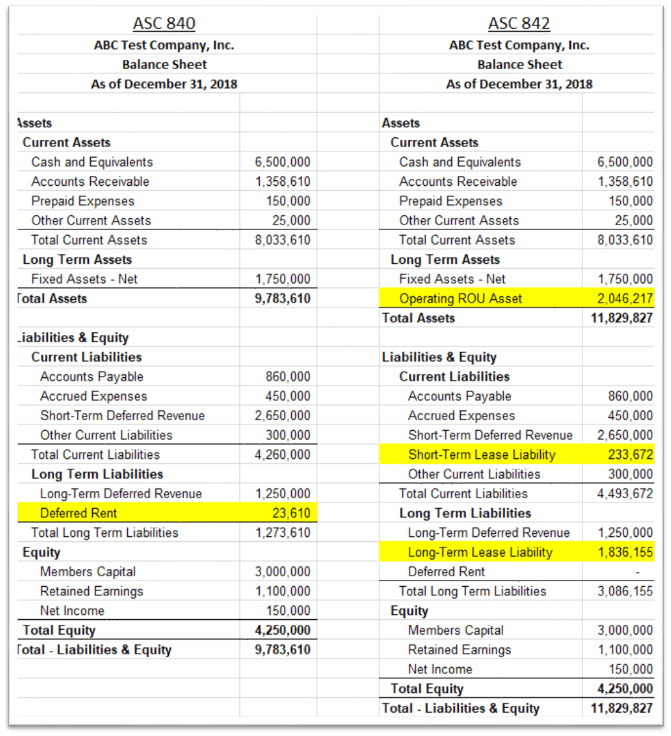

Operating Leases on the Balance Sheet Example

Here’s an example of a balance sheet for 840 and a balance sheet for 842. Both represent the same operating lease data.

In this example, we have included only a single operating lease. It’s a real estate lease with an initial lease term of January 1, 2018 to December 31, 2025. The rent starts out at $27,000 per month, and increases 2% each year until it gets to the final amount of $31,014.51. For the sake of simplicity, we do not have any prepaid rents, initial direct costs, or lease incentives on this lease.

As you can see, under ASC 840, we have a very small deferred rent balance of $23,610 as of 12/31/18. Our Total Assets are only about $9.8 million and our Total Liabilities are only $5.5 million. Realistically, we have a future cash obligation on this lease of almost $2.5 million dollars, but the only way we would see that under 840 is if we dug into the disclosure report and looked at the maturity analysis. And remember, even the maturity analysis is not a fair representation of our actual liability, because of the time value of money.

Looking at the same example under ASC 842 (using a 5% discount rate), you can see a very different impact on the balance sheet.

To provide an apples-to-apples comparison with 840, we are capitalizing this lease on 1/1/18 and not transitioning. Our net present value of payments, which is the starting point for your lease liability, is almost $2.3 million.

As of 12/31/18, you can see that we have a total right of use asset of $2,046,000, and a total lease liability of $2,069,000 (including both short term and long term lease liability). Our Total Assets for the year went from about $9.8 million to $11.8 million. Our Total Liabilities went from $5.5 million to about $7.6 million.

For this example, there’s no change to the P&L. Our straight line rent expense under ASC 840 is $347,610 for 2018. Under ASC 842, the total lease expense is the same, but $239,000 is related to amortization, and $108,000 is related to interest expense. For 2018, we’ve made $324,000 in payments, but only reduced the liability balance by $216,000.

Keep in mind that the impact on this balance sheet represents only a single 5-year real estate lease. When you extrapolate this out to an entire property portfolio, and also capitalize any equipment leases you may have, the balance sheet impact will be much, much larger.

5. How has lease classification changed under ASC 842?

Upon adoption of ASC 842, almost all leases will be capitalized on the balance sheet. However, you will still need to classify them as either finance leases (previously called capital leases) or as operating leases using the lease classification test so that you can apply the correct accounting treatment.

Lease Classification Test

The lease classification test questions determine whether the leased asset is essentially owned as well as controlled by the lessee. If so, the lease must be classified as a finance lease. If the lessor retains ownership, the lease must be classified as an operating lease. So if the lease is non-cancelable and you answer YES to one or more of the lease classification test questions, then the lease is classified as a finance lease.

These four lease classification test questions remain the same as ASC 840:

Transfer of title test: By the end of the lease term, will ownership of the asset transfer from the lessor to the lessee?

Bargain purchase option test: Is there a purchase option in the lease that the lessee is reasonably certain to exercise?

Lease term test: Does the lease term encompass the major part of the remaining economic life of the underlying asset?

Present value test: Is the present value of lease payments plus RVG (residual value guaranteed by the lessor) greater than or equal to substantially all of the fair market value of the asset?

A fifth test question has been added in ASC 842:

Alternative use test: Is the asset so specialized that it is only useful to the lessee? This new test question means that after the asset is returned to the lessor, will it have no value to anyone else without a major overhaul by the lessor?

You may have noticed that the “bright lines” for lease classification tests have been removed in ASC 842. Previously they indicated what percentage constitutes a “major part” of economic life (75%) or “substantially all” of the fair market value (90%). These are now considered guidelines under the new standard and you can elect what percentage you choose to use.

In the past, it was easy to manipulate this number and classify more leases as operating leases (which did not need to be capitalized). Under ASC 842, all operating leases are recorded on the balance sheet anyway, so there’s no reason to do this.

6. How is lease liability calculated under ASC 842?

Lease liability is calculated as the Present Value of minimum future lease payments. You will need to make assumptions about the probable amounts owed under residual value guarantee, and also whether you are reasonably certain to exercise renewal options, termination options, and purchase options, because exercising these options impacts your minimum future lease payments.

Things to consider:

- Discounting Future Payments: Since lease payments occur over time, they must be discounted to present value using the appropriate discount rate. The discount rate to use for the calculation is either the rate implicit in the lease (if known), or your organization’s incremental borrowing rate.

- Impact of Lease Term Assumptions: If a company is reasonably certain to exercise renewal or purchase options, those additional lease payments must be included in the calculation.

- Remeasurement Adjustments: It’s important to remember that the assumptions you make at the inception of the lease (about whether or not you will exercise options) can and often do change over time. When those changes happen during the term of a lease, you will need to remeasure both your lease liability and your ROU asset. Remeasurements may also be needed due to abandonments, asset impairments and other causes.

7. How do you calculate ROU?

To calculate the ROU asset, start with the lease liability and then adjust for additional costs or benefits related to the lease.

- Start with the Lease Liability – This is the present value of all future lease payments.

- Add:

- Initial Direct Costs – These are costs directly tied to negotiating or executing the lease, such as legal fees or broker commissions.

- Prepaid Lease Payments – Any lease payments made before the lease officially begins.

- Subtract:

- Lessor Incentives – Any payments or reimbursements received from the lessor, such as tenant improvement allowances.

- Accrued Rent – If rent has been incurred but not yet paid at transition.

- ASC 420 Liability at Transition Date – Any existing liability from previous lease accounting adjustments, such as restructuring costs.

All of these assets and liabilities that adjust the ROU asset are now reclassed from the balance sheet and included as one number to show the total leased asset.

8. What is an embedded lease?

Accounting for embedded leases represents one of the trickier aspects of implementing the new ASC 842 standard. Simply put, embedded leases are components within contracts that entail the use of a particular asset, where the user has control over that asset. A lease may exist within a contract even though the contract may not contain the word “lease.”

For example, embedded leases are commonly found in IT service contracts, where a vendor may provide specific equipment (such as on site servers). They are also frequently found in supply contracts, dedicated manufacturing capacity contracts, and advertising agreements (such as use of billboards).

You may have done some embedded leases accounting in the past, and the process has not changed much in ASC 842. However, this is now a significant issue because embedded leases have a much bigger impact on your income statement under the new rules.

Under ASC 840, operating leases were off balance sheet, so any embedded leases had an immaterial impact to the income statement since the expense was probably being straight lined anyway.

ASC 842 requires ALL leases to be capitalized on the balance sheet, including all embedded leases. That means you will need to examine your contracts to find any embedded leases within them, and you will need to separate the lease components (for use of assets within a contract) from non-lease components (payments for the service) within these contracts.

This is a complex and time-consuming task, so be sure to allocate the necessary time and resources to get it done. It also involves making judgments, so it’s imperative that people doing this work are experienced with leases and understand the standard. Also, you must document your policies and procedures to support your decisions and to provide justification for future audits.

How to identify an embedded lease

As you review the content of your existing contracts, ask these questions to decide (ideally with the guidance of your advisory partners) if they contain embedded leases:

Does the agreement entail the use of one or more specific assets?

If no assets are specified, then no lease can exist within the contract. However, if an asset is explicitly or implicitly identified within an agreement, then a lease may exist.

- “Explicit” means the asset is identified on the contract, such as by a serial number or VIN number.

- “Implicit” means use of a specific asset is implied even if not explicit, such as when the supplier can’t fulfill the contract with any other asset for legal or economic reasons.

For example, power purchase agreements may include the use of a specified plant. Oil and gas drilling contracts may specify the use of equipment and pipelines.

Is the asset physically distinct?

For a lease to exist, a specified asset must be a physically distinct object. Something intangible, such as exploration rights, cannot be considered an asset. A biological entity also cannot be considered an asset under 842.

Does the supplier have substantive substitute rights for the asset?

If your agreement does specify the use of an asset, can the supplier easily substitute a different asset, and would the supplier benefit from doing so?

- If the supplier can substitute the asset and benefit economically by exercising that right, a lease may not exist in the contract.

For example, if a supplier uses trucks to ship materials and has the ability to substitute different trucks (with a smaller or larger capacity as needed), then there is no lease.

- If the supplier can’t substitute the asset and would not benefit from doing so, then the use of that asset may be considered a lease.

For example, managed services contract might include office copiers. It’s not likely that the supplier can easily swap out one machine for another. And it’s also not likely that the supplier would benefit financially from doing that even if they could. In that case, the use of the office copier would constitute a lease.

Does the customer obtain the economic benefit from using the asset?

If you as the customer get substantially all of the economic benefit from the use of the asset, then your use of that asset may be considered a lease.

Common practice is to interpret “substantially all” to mean greater than or equal to 90% of the economic benefits of the asset.

Can the customer direct use of the asset? If you have physical control and decision making authority over when and how the asset is used throughout the period of the lease, then a lease may be present.

Ready to simplify your lease accounting? Learn how Visual Lease helps you manage data, improve accuracy and stay compliant.

Ready to strengthen your ASC 842 compliance? Learn how Visual Lease helps you centralize lease data, improve reporting accuracy, and manage lease accounting with confidence.