How ASC 842 Treats Different Lease Terms Organizations are increasingly seeking flexible lease options, with short-term leases, leases with a maximum term of 12 months or less, becoming more popular....

Read More

How often do you have this experience when evaluating enterprise software? The vendor gives a demonstration of an amazing solution, walking you through complex tools that do exactly what you…

Lease accounting is a massive, cross-functional effort. It involves various stakeholders and systems that impact (and are impacted by) leases. It is not just an accounting problem – and goes…

What are rent concessions? Rent concessions are discounts, incentives, or other benefits provided by landlords to tenants. Landlords sometimes offer rent concessions to entice tenants to sign a new…

Visual Lease, LLC (hereinafter “VL,” “we,” “our,” and “us”) appreciates being given an opportunity to comment on the Exposure Drafts published by the International Sustainability Standards Board (hereinafter the “ISSB”)…

Visual Lease, LLC (hereinafter “VL,” “we,” “our,” and “us”) appreciates being given an opportunity to comment on the Exposure Drafts published by the International Sustainability Standards Board (hereinafter the “ISSB”)…

Lease inventories, hiring more staff and renegotiating lease terms are some of the moves private companies can take to make compliance easier.

The FASB on Sept. 21, 2022, voted by 4 to 3 to issue a proposal that would change the accounting rules for leasehold improvements in inter-company leases done by both…

FinLedger spoke with Joe Fitzgerald, senior vice president of lease market strategy at Visual Lease to discuss the report and understand the implications of the new lease accounting standards.

PropTech Breakthrough, an independent market intelligence organization focused on real estate and property technology companies, yesterday announced its second annual PropTech Breakthrough Awards, highlighting some of the most influential and innovative…

The Financial Technology Report is pleased to announce The Top 25 Financial Technology Leaders of New Jersey for 2022. While New Jersey may be considered part of the New York…

Real estate is one of the largest operating expenses for retailers worldwide. Second only to labor costs, rent can account for more than 30 percent of expenses and, according to research from…

Even though leases typically comprise a major piece of a business’ budget, most companies don’t know how much their leases cost and many are unsure about how to account for…

The new lease accounting standards under ASC 842 are sticky, demanding, and—after multiple delays—most definitely here for all companies, whether public or private when the Financial Accounting Standards Board finally…

The new lease accounting standards under ASC 842 are sticky, demanding, and—after multiple delays—most definitely here for all companies, whether public or private when the Financial Accounting Standards Board finally…

As part of my series about the “5 Things You Need To Know To Create a Successful App or SaaS”, I had the pleasure of interviewing Marc Betesh. Marc Betesh…

Professionals on the Move is a round-up of recent staffing announcements and promotions in and around the tax and accounting space. Carrie Summerlin Named FICPA’s New Chief Growth & Innovation…

The introduction of lease accounting standards has forever altered how public, private and government entities manage, track and report on their leases. To understand more about the leasing sector and…

In response to the ongoing impact of the global pandemic on revenues and business operations, companies are evolving how they prioritize and manage their commercial real estate leases. Many organizations…

Company achieves double-digit YoY annual recurring revenue, customer and employee growth Woodbridge, NJ – April 18, 2022 — Visual Lease, the #1 lease optimization software provider, today announced results from…

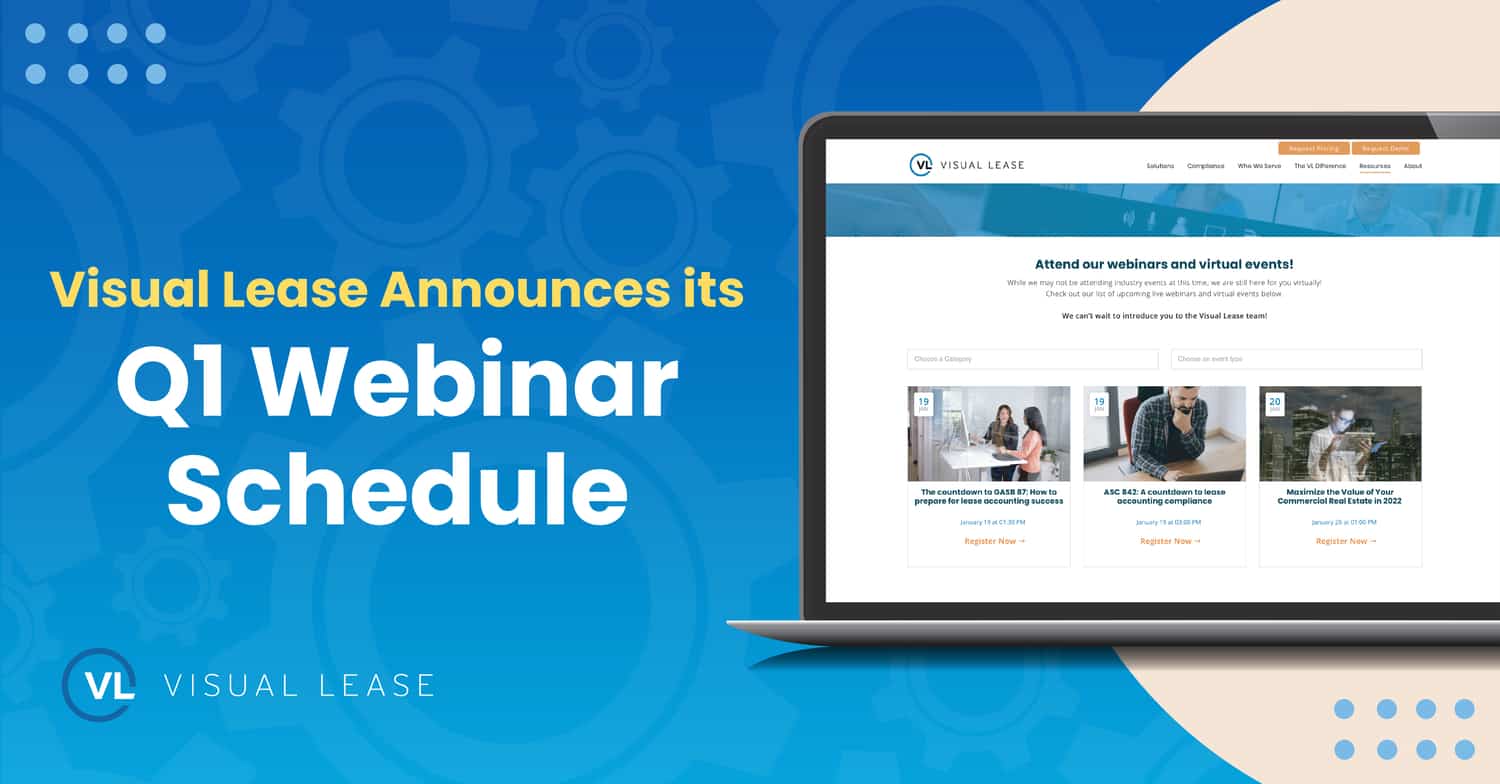

Industry leader continues to host virtual events to help companies master lease accounting compliance Woodbridge, NJ – April 12, 2022 —Visual Lease, the #1 lease optimization software provider, announced its…

The standard in some ways parallels the ASC 842 leases standard for public and private companies and nonprofits from the Financial Accounting Standards Board and the IFRS 16 leases standard…

The introduction of new lease accounting standards (ASC 842, IFRS 16 and GASB 87) has had a significant impact upon accounting and reporting for U.S. publicly traded and private companies,…

The past two years have shuffled business priorities and workflows, which has left many companies catching up on their transition to the new lease accounting standards (ASC 842, GASB 87,…

Company achieves double-digit YoY annual recurring revenue and customer growth for fourth consecutive year Woodbridge, NJ – January 20, 2022 — Visual Lease, the #1 lease optimization software provider, today…

Industry leader to host a series of virtual events, sharing valuable insights to help companies master lease accounting compliance Woodbridge, NJ – January 11, 2022 —Visual Lease, the #1 lease optimization software…

Lease accounting compliance is not just a one-and-done disclosure. It is a new approach to accounting that includes an ongoing, cross-departmental effort – and a much higher level of scrutiny….

In a 2020 IDC survey, 42% of technology decision makers reported that their organizations planned to invest in technology to close the digital transformation gap. We expect that number has…

There is power within your lease portfolio. Over the last year, public and private businesses have taken a closer look at their leases – and experienced the downstream benefits of…

Last year, the Financial Accounting Standards Board (FASB) provided private companies with an extra year to adopt lease accounting standard ASC 842. When this was announced, 63.8% of surveyed private company executives…

This article originally appeared here in Forbes. As a result of Covid-19 and the changing landscape related to leases, private companies have received more time to prepare for and adopt…

This article originally appeared here in Forbes. In 2020, many companies were forced to make tough decisions regarding their leased commercial spaces. From office closures to consolidations and deferrals, many…

What is an embedded lease? Simply put, embedded leases are components within contracts that entail the use of a particular asset, where the user has control over that asset. You…

Hundreds of private organizations have begun their journey towards lease accounting compliance. Although, many of them underestimate the amount of effort involved with preparation. In particular, assembling a team…

Although private companies still have some time to adopt the new lease accounting standards, public companies have already had to meet their compliance deadlines. In doing so, these companies have…

Recently, we have talked a lot about ways that companies can understand their lease obligations and reduce costs in light of COVID-19. What many businesses have discovered during this time…

Across industries, sectors and organizations of different sizes, the COVID-19 outbreak has touched virtually every business in some way. Between stay-at-home orders, emergency closures, and supply chain disruptions, companies are…

With all the business closures and cutbacks due to the COVID-19 pandemic, a lot of companies are worried about not only managing their lease expenses now, but also accounting for…

Deciphering financial and contractual obligations of a lease can be a challenge. And that is especially true during an unprecedented event, such as the COVID-19 pandemic. All you really want…

The COVID-19 pandemic has impacted every company in some way. With “social distancing” and all the emergency regulations that are in place, many offices and nonessential businesses are shut down…

In an act of relief for companies during the coronavirus pandemic, the Financial Accounting Standards Board (FASB) recently voted to propose a one-year deferral of major accounting standards, including ASC…

With all the new lease accounting rules you have to contend with — whether you follow ASC 842, IFRS 16, or GASB 87 — the prospect of generating lease accounting…

With the big push to achieve compliance, a lot of businesses have been laser-focused on making the transition to the new FASB/IFRS lease accounting requirements. While that is understandable, it’s…

As the standard for lease accounting software, Visual Lease provides the tools you need to achieve compliance. We make it easy to track, report, and manage your lease finances within…

The challenges of lease accounting data collection for distributed firms Getting ready for compliance with the new lease accounting standards (FASB ASC 842 and IFRS 16) is a complex and…

Can your lease accounting software find lease payment mistakes? Were you under the impression that lease accounting software could only perform accounting calculations and add information to your balance sheet?…

Visual Lease, a New Jersey-based lease management and accounting SaaS company, today announced Clark Convery joined its team as Chief Operating Officer. Prior to Visual Lease, Convery was General Manager of the Enterprise…

Achieve fast compliance and long-term value with Grant Thornton and Visual Lease’s joint lease accounting solution With the enactment of the new IFRS 16 & ASC 842 (FASB) lease accounting…

With FASB compliance less than a year away, Visual Lease is doing all we can to smooth the transition — including delivering a new lease accounting update designed to make…

For corporate real estate decision-makers, will the new lease accounting standards make an already challenging job even more difficult? You already have many factors to consider when choosing locations, negotiating…

A key process for the CRE executive is overseeing the site selection process, particularly for major office, data center, or manufacturing sites. I’m going to focus on office site selection since this typically represents the most frequent type of leasing actions.

It was early summer of 1995, and I was aboard a French SST Concord traveling at roughly Mach3 from New York to Paris..

The long awaited new lease standard has arrived! The International Accounting Standards Board (IASB) released its version of the new lease standard last week with implementation scheduled for early 2019. The US accounting standards board (FASB) is expected to release its version shortly with implementation to follow soon after IASB’s.

With the New Year it’s a good time to take stock of the corporate real estate domain and consider the challenges facing the managerial profession responsible for the corporation’s real estate assets and services in the year ahead. Here are five major challenges if dealt with effectively will determine in part the success of corporate real estate in 2016.

In a earlier white paper, The Lease Accounting Tsunami; Are You Prepared to Weather the Storm?, I wrote that users should evaluate the effects of the new FASB/IASB on a company’sdebt structure, debt to equity, and other factors that would be affected by the new standard, assuming lease liabilities would be considered as debt. In point of fact, the FASB explicitly decided that Type B lease liabilities should not be considered as “debt.” However, the IASB which treats all leases as Type A leases or capital leases, does consider these liabilities as “debt-like liabilities.” (Their exact words) As one of my accounting friends advised “The accounting for Type A leases requires IASB companies to record interest expense, and segregates payments on the lease liability into operations and financing outflows per the cashflow statement, which is consistent with debt.”

Thus, US companies will experience less impact from the new standard, particularly as it relates to debt covenants, debt to equity metrics, and capital structures. But US companies with significant international lease portfolios subject to the IASB standard, will see their debt levels increase.

We are frequently asked why we need a new FASB lease standard.. here are our thoughts…

There’s compelling logic to combine a lease audit service with a lease management system such as Visual Lease..