Lease subleasing might seem like a niche topic, relevant only to companies deeply entrenched in real estate dealings. However, it impacts more businesses than one might think. Whether you’re a tenant looking to downsize your space or a landlord exploring income diversification, understanding the nuances of lease sublease accounting (especially under ASC 842) is crucial.

The Basics of Lease Sublease Accounting

Many companies, despite primarily being tenants, may find themselves with excess space at certain points in their business cycle. To mitigate lease obligations or generate additional income, they often turn to subleasing arrangements. Traditionally, under ASC 840, sublease income was treated as a reduction in lease expenses. However, ASC 842 introduced significant changes.

Under ASC 842, sublease accounting becomes more intricate. The key distinction lies in whether the original lessee (now acting as a sublessor) remains liable to the superior landlord for the full lease amount. If so, the sublease income isn’t a direct offset to lease expenses but rather recognized separately as income. This shift ensures transparency and accuracy in financial reporting, aligning with the principle of faithfully representing financial transactions.

Key Considerations in Sublease Accounting

Separate Transactions

ASC 842 mandates that sublease transactions be treated distinctly. The sublessor must account for their ongoing lease obligation to the superior lessor separately from the income received from the sublessee.

Impact on Financial Statements

Unlike under ASC 840, where sublease income offset lease expenses directly, ASC 842 requires the sublessor to maintain both lease liability and recognize sublease income independently. This approach reflects a more accurate representation of financial positions and obligations.

Legal and Administrative Aspects

Subleasing often requires landlord consent and adherence to lease terms. Administrative tasks, such as ensuring compliance with lease conditions and obtaining necessary approvals, add complexity but are vital for legal and operational continuity.

Related Party Transactions

Special rules apply when subleasing to related parties. Both IFRS and US GAAP have specific requirements for how these transactions are accounted for, emphasizing clarity and fair representation.

Sublease Accounting Practical Examples and Implications

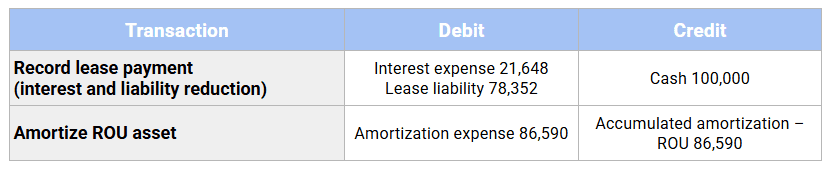

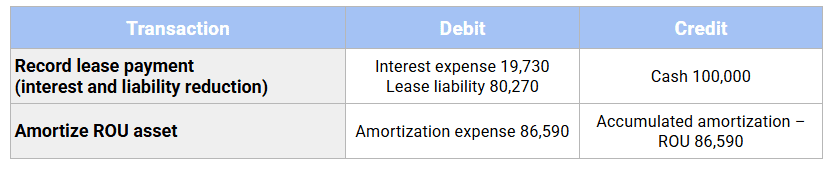

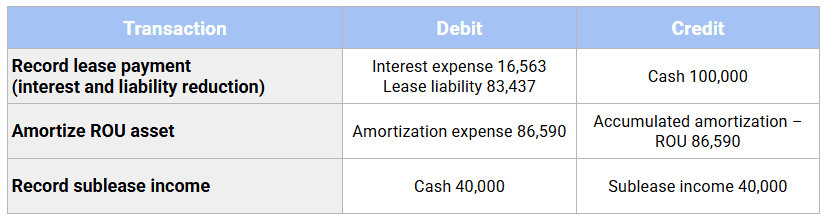

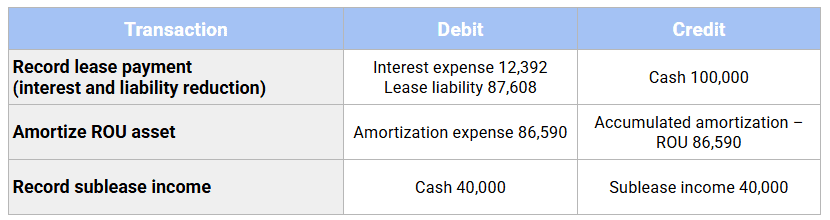

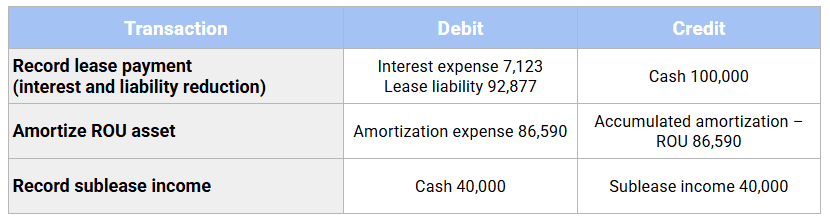

When a company subleases part of its leased space, the accounting can appear complex. Under ASC 842, the original lease obligation does not change, but the sublease is treated as a new, separate agreement. This means the company continues recording lease expenses for the full head lease while also recognizing sublease income once the sublease begins.

To make this easier to follow, the example below walks through each year of a five-year office lease, showing the journal entries for both the head lease and the sublease (starting in Year 3). A summary table at the end highlights the net effect on the income statement.

Year 1

Year 2

Year 3

Year 4

Year 5

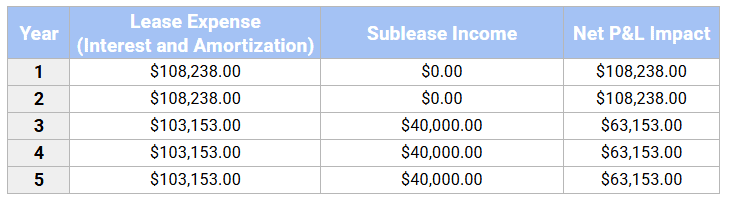

Summary View of Lease and Sublease Accounting

The table below summarizes the total lease expense, sublease income, and net impact on the income statement across the five-year term.

The Net P&L Impact is simply the difference between the company’s total lease expense and any sublease income received in a given year.

Termination and Amendments

Terminating a sublease or negotiating changes can also impact financial reporting. Whether terminating both the sublease and the superior lease or just one, each action requires careful consideration of asset write-offs, liability adjustments, and potential gains or losses.

International Differences

IFRS and US GAAP may differ in how they treat certain aspects of sublease accounting, especially concerning related party transactions. Understanding these nuances is essential for companies operating across different jurisdictions.

Sublease Accounting Under ASC 842

Lease sublease accounting under ASC 842 represents a significant departure from previous standards, aiming to enhance transparency and accuracy in financial reporting. It requires companies to carefully track lease obligations, sublease income, and comply with legal requirements to avoid potential pitfalls.

By adhering to these guidelines and understanding the intricacies of lease sublease accounting, businesses can navigate financial complexities more effectively, ensuring compliance and maintaining robust financial health.

In summary, while lease sublease accounting may seem complex, especially under ASC 842, it’s a critical aspect of financial management for companies with lease obligations. Staying informed and implementing sound accounting practices ensures companies can optimize their leasing strategies while meeting regulatory requirements effectively.

Lease and Sublease Accounting Frequently Asked Questions

Does a sublease reduce the original lease liability under ASC 842?

No. The head lease liability remains unchanged because the original lessee is still legally obligated to the landlord. The sublease is recorded separately.

How is sublease income reported in the financial statements?

Sublease income is typically recognized as lease revenue (or other income) on a straight-line basis over the sublease term. It is not netted against lease expense.

What determines whether a sublease is classified as operating or finance?

The same classification tests apply as for any lease under ASC 842 (e.g., transfer of ownership, present value test, major part of economic life). Most subleases of office space are operating leases.

What happens if the sublease covers the entire leased property?

The accounting is the same — the original lease liability remains, but now the company may effectively act as an intermediary landlord. Disclosure of sublease terms becomes especially important.

How do subleases affect lease disclosures under ASC 842?

Both the head lease and the sublease must be disclosed separately. Organizations need to show lease liabilities, ROU assets, lease costs, and lease income in their notes.

Can sublease income offset lease expense on the income statement?

No. ASC 842 requires gross presentation. Lease expense is shown as incurred, and sublease income is recognized separately.